Who was Paul and why did he sue Virginia?

Who was Paul and why did he sue Virginia?

The story behind the SCOTUS Decision in Paul v Virginia, which shaped insurance public policy for 75 Years.

Countless continuing education programs for insurance producers cite the historic case of Paul v. Virginia 75 U.S. (8 Wall.) 168 (1869) but very few instructors take the time to explain: Who the heck was “Paul” and what was his beef with the Commonwealth of Virginia?

The 1869 Supreme Court of the United States (SCOTUS) decision in Paul formed the cornerstone of American insurance law for 75 years. Contrary to the hopes of the litigants who brought the case to the federal courts, the decision established state jurisdiction over the “business of insurance.”

Apart from the case’s legal importance, the story of Paul is interesting because it is also a cautionary tale of human folly and unintended consequences.

The case was a political gamble, which went terribly wrong for the insurance executives who threw the dice.

Unfettered Competition

The narrative of the Paul decision begins with the formation of the New York Underwriters Agency (NYUA): a fire insurance cartel. Readers will keep in mind that in the mid-19th Century “cartel” was not yet a derogatory term. Insurance executives formed the NYUA to temper the destructive aspects of unfettered competition.

Today, insurance lobbyists deliver testimony that pines for deregulation to legislative and regulatory bodies, their pleas run counter to insurance history. Never in history did insurers want a deregulated or competitive market. Left to its own devices the insurance sector created institutions for private control of product design and pricing.

As early as the 1820s, states began establishing regulatory agencies to oversee aspects of the insurance business. Yet, as we shall discuss in future posts, these agencies tended to establish rules aimed at protecting local companies and policyholders. As insurance firms grew into multistate business concerns, the state-based system proved ineffective and inefficient.

In the absence of national regulation, or coordinated state-by-state regulation, insurers created a private regulatory system. That private system consisted of regional cartels. Those cartels attempted to nationally coordinate their operations to privately regulate the business of insurance through a national trade association.

In the years prior to the Civil War, unfettered competition drove the price of fire insurance so low that insurer insolvency was a regular occurrence. Competition made pricing the risk of financial loss next to impossible.

While the notion of low prices sounds like a Consumer Paradise, property owners too often paid for insurance coverage that they could never make claims upon because the insurer that issued the policy failed. The consumer not only suffered monetary loss from fire, wind, or other covered peril, but also suffered loss of premium payments paid to an insolvent insurance carrier.

The problem of fire insurers failing arose from multiple elements: including (but not limited to) imperfect actuarial practices, inadequate loss data, geographic concentration of company marketing efforts, as well as overzealous sales agents and underwriters.

Furthermore, the use of predatory pricing, designed specifically to drive competitors out of the market, or out of business, led to the failure of both the predatory firm and its prey alike.

This unregulated market produced low prices but demanded redundant purchases. For example, in the 19th Century, a smart fire insurance consumer never insured a structure with just one company. Property owners “stacked” policies from multiple companies. An informed consumer never insured more than 20 or 25 percent of the worth of a structure with a single company – in the hopes that three or four of the companies may remain solvent to pay claims. (Remember, insurance guaranty associations would not widely exist to pay claims against failed companies until the late 1960s.)

Fire insurance was undependable. Insurers were unable to earn the public confidence – a fatal flaw for a business based on trust.

The Cartels

Private regulation of insurance arose from the activities of urban Chambers of Commerce as early as the late 18th Century. Still, these arrangements proved parochial and ill-suited for regional or national operations.

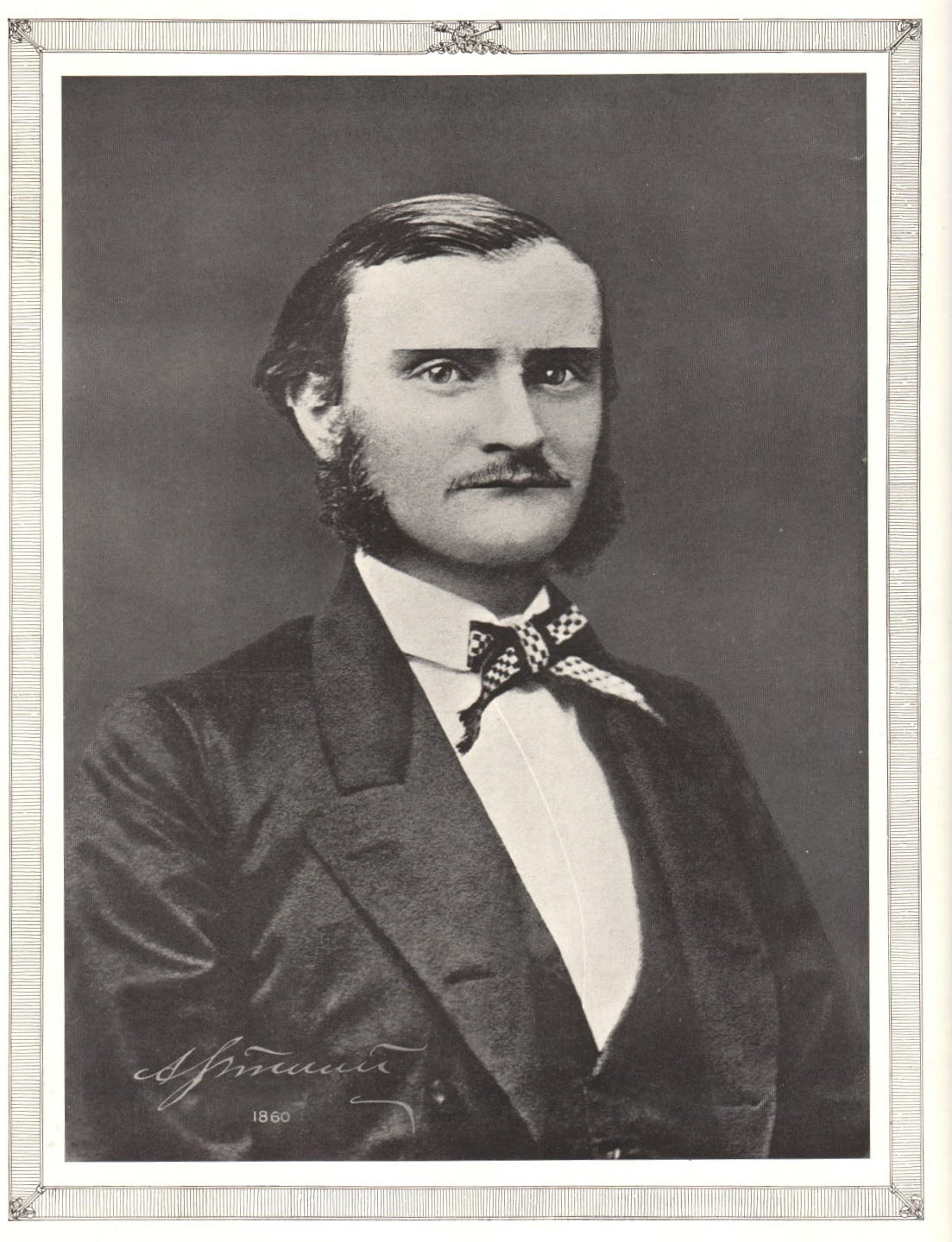

Alexander Stoddart, a Scottish immigrant who sold fire insurance in the Mississippi Valley prior to the Civil War, was a transformative figure in the private regulation of fire insurance. He would have been familiar with the cooperation among fire insurance carriers in the St. Louis area.

Around the beginning of the insurrectionist violence, Stoddart moved to New York City. He mulled over an idea based on a corporate organization that he hoped would discipline unruly practices that undermined trust in fire insurance.

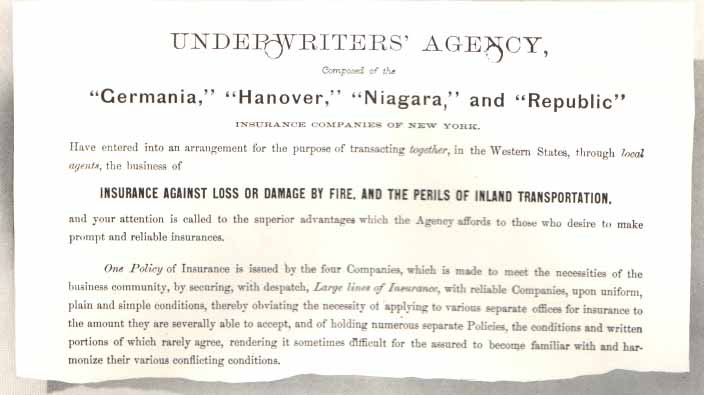

On May 1, 1864, Stoddart founded the NYUA, a cartel agreement consisting of four insurers: Germania, Niagara, Hanover, and Republic Insurance Companies. Participating companies offered a uniform fire policy form at a single policy rate. Each company assumed an equal part of the risk transferred by every policy.

By forming the cartel, the NYUA endeavored to make fire insurance dependable in two ways: restraining competition and spreading the risk of loss.

Readers may find it interesting to note that Stoddart and the NYUA predates John D. Rockefeller’s first attempt to “harmonize” the petroleum sector through The South Improvement Company (1871-1872).

Stoddart’s cartel offered secure coverage and a reasonable rate – at least, at the beginning, A company history claims that the cartel passed efficiency-based cost savings along to their policyholders. The marketplace rewarded the Stoddart’s cartel, and he expanded his operations into the Midwest and Upper South.

Business expansion brought the Stoddart organization in contact with an increasing number of state government jurisdictions. As previously noted, state jurisdictions tended to enact parochial rules designed to protect and serve local business interests. This parochialism frustrated Stoddart. It was as if the United States never threw out the state compact-oriented Articles of Confederation, and never adopted the federal Constitution to make one nation – and one market.

Local regulation of a national business concern presented a complex problem and Alexander Stoddart viewed himself as an analytical person capable of solving that problem. He and his team of cartel administrators possessed confidence that if they could conquer competition, they could conquer parochialism.

One Set of Rules

Stoddart pursued a national system of regulation. The feisty Scot was convinced that a national business could not operate under a patchwork of local rules. Stoddart wanted one set of rules, and if those rules did not “fit” a particular carrier’s business model – so be it. Furthermore, at that time, the federal government was both underfunded and undermotivated to be a nuisance to the fire insurers.

According to a 1914 NYUA publication: “Insurance men foresaw the difficulties which ultimately materialized: conflicting state laws, unequal and onerous taxation and ill-considered legislation directed against principles the observance of which was essential to correct conduct of the business of the day and period.”

Initial success came when Stoddart won a ruling from the Internal Revenue Bureau, which ruled the sale of the cartel’s four-company policy form as a single transaction.

This victory meant that the federal revenue bureau would only require a single “tax stamp.” The ruling strengthened the cartel’s contention that it should operate under a single set of federal rules in the stream of interstate commerce.

In 1866, Stoddart’s cartel worked with the newly established “National Board of Fire Underwriters” (NBFU), a trade association, to lobby Congress in support of National Insurance Bureau legislation. The proposed Bureau would issue federal charters to insurers modeled upon the national banking charters created by the National Bank Act of 1863. A federal charter would remove “national insurers” from state-by-state jurisdictions.

The legislation stalled in the US Senate. Remember, at that time, the state legislatures elected US Senators, so any proposal that tended to lessen the jurisdiction of those legislatures faced an uphill battle.

Litigation

In response to the stalled legislation, Stoddart concocted a plan to win in the federal courts by having an agent of the cartel refuse to pay a state-licensing fee resulting in the termination of his license. Once terminated by the state, the unlicensed agent would openly sell insurance coverage in defiance of state law.

State action against the NYUA agent would give the cartel standing in federal court to bring suit challenging the state’s jurisdiction.

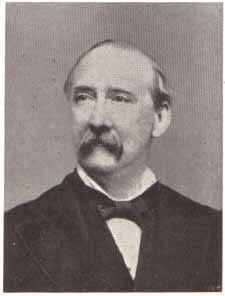

The cartel looked to Petersburg, Virginia, and Colonel Samuel B. Paul. The NYUA called upon Colonel Paul, who was both a sales agent and lawyer for the cartel, to execute the plan. Col. Paul violated Virginia’s licensing law as planned. When the state launched an enforcement action against Paul, the NYUA filed a complaint in federal court in their unlicensed agent’s name.

Now, one may assume that the NYUA complaint in federal court would focus on the Commerce Clause of the Constitution; Article 1, Section 8, Clause 3. The Commerce Clause achieved a primary aim of the Federalists who drafted the Constitution: The placement under the jurisdiction of the national Congress the power to regulate commerce across state lines. The constitutional clause delegates to Congress the power “to regulate commerce with foreign nations, and among the several states, and with the Indian tribes.”

Nevertheless, the NYUA complaint initially ignored the Commerce Clause.

Instead, the NYUA argued that Virginia abridged the citizenship rights of NYUA as a corporate citizen of New York. The cartel argued that this abridgement violated its Constitutional right to equal protection under the law. The odd legal argument initially showed promise, the trial court found for the cartel.

The commonwealth appealed.

Before the appeals court the cartel augmented its argument to include the Commerce Clause. In addition to the citizenship claim, the cartel argued that state regulatory frameworks unconstitutionally preempted federal jurisdiction over interstate commerce.

The appeals court rejected both NYUA arguments. The appellate decision overturned the trial court and found for the Commonwealth of Virginia.

The NYUA appealed to the SCOTUS and the NBFU joined the legal team. On behalf of the insurers, J.M. Carlyle of Washington, D.C., and former Supreme Court Justice B.R. Curtis of Boston presented arguments to the Court.

To the great surprise of the insurers, the SCOTUS upheld the appeals court decision in favor of the Commonwealth of Virginia.

The unanimous opinion rejected the citizenship rights argument on the grounds that corporations were not natural citizens and therefore could not benefit from citizenship rights – which is a far more rational opinion than holds sway on today’s “Roberts Court.”

Then, the SCOTUS deeply imbibed from the Cup of Weird Reasoning. The SCOTUS dismissed the insurers’ interstate commerce argument. The Court opined that insurance was not commerce; therefore, state regulation of insurance did not wrongfully preempt the Congress’s constitutional jurisdiction over interstate commerce.

In short, if an activity was not commerce, then it could not be interstate commerce. Congress only had jurisdiction over interstate commerce, so the Court found for the Commonwealth of Virginia.

Why did the Court “go there?” We really do not know; however, in the late 1860s the SCOTUS membership consisted of a conservative majority. Antebellum social conditions shaped their jurisprudence, which reflected the pre-war deference to “states’ rights” to defend slavery and White Supremacy.

Around the time of the Paul Decision, the conservative majority on the court issued a series of decisions that bent over backwards to deny SCOTUS approval for increasing federal jurisdiction, in any way.

From an historical viewpoint, we can infer that the conservative Court majority sought to strike down the fire insurers’ attempts to invite federal oversight to resist expansion of the federal role in American society – at a time when congressional majorities labored to destroy the state-based, Antebellum, social systems based upon White Supremacy.

The decision in Paul v. Virginia would shape American insurance law until the SCOTUS overturned the insurance provisions of the Paul Decision in United States v. South-Eastern Underwriters Association (SEUA), 322 U.S. 533, (1944). In the latter decision, Justice Hugo Black wrote for the Court’s majority that insurance is commerce and is interstate commerce; therefore, it falls under the Commerce Clause’s definition of congressional jurisdiction. But readers may exclaim: Wait, the states regulate the business of insurance!

In 1945, the Congress made a limited and contingent loan of that jurisdiction to the states through passage of the McCarran-Ferguson Act (PL 15 of 1945). Congress and the Roosevelt Administration intended the McCarran-Ferguson Act to provide a temporary “moratorium” on application of federal antitrust law and fair-trade oversight, to the extent that state law provided affirmative regulation of those areas. The statute remains the law of the land to this date of this post.

But that tale of what led to McCarran-Ferguson is the topic for future editions of Savage Tales of Genuine Risk.