Winds of Change

In the decades between the American Civil War and World War II, a system of private cartels regulated prices and product design in the fire insurance sector. The anticompetitive network of local and regional organizations consisted of stock-funded fire insurers.

Life insurers did not join the cartel but coordinated the sector’s activities through interlocking boards of directors and bank relationships. Mutual insurance companies were outcasts because they usually served geographic regions or demographic groups that the stock insurers rejected out of arrogance or ignorance.

On October 5, 1943, Wendell Berge, a senior lawyer at the US Department of Justice (1941-1946), described the political power of the fire insurance cartels in a memorandum for Attorney General Francis Biddle, as follows:

Masquerading in the white robes of States Rights, with an inspired lobby of Governors as shock troops and the far-flung system of fire insurance organizations as heavy artillery, the insurance companies have audaciously opened an offensive for special priviledge [sic] which, unless it is promptly and effectively combated, will deliver the insurance buying American public completely into their hands.

At the time of Burge’s writing, the insurance lobby was promoting bills in Congress to exempt it from the Sherman and Clayton Anti-Trust Acts if the Supreme Court overturned the finding in the Paul v. Virginia decision that opined that insurance was not interstate commerce.

Authoritarian Power

It is difficult to exaggerate the political power at the state and local level of the fire insurance cartels in America. The cartels extension or retention of risk transfer to businesses, placed a commercial governor on the engine of construction and industrial expansion. The insurance sector gave or withheld financial investment and employment – including a network of well-connected sales agents distributed across every state – imbued the cartel and its companies with economic importance, which was easily convertible to political power.

Cartels, and the National Bureau of Fire Insurance (NBFU), bore no qualms about using that power. The cartels exerted control over building codes, firefighting, water services and other policy matters in American cities and many towns. For example, in Kansas City, Missouri, a private for-profit water company failed to expand its acquisition system to match the growth of the city. The distribution system could not deliver water with adequate pressure, which the local fire cartel (The Fetter Bureau) deemed necessary to fight fires. So, the Fetter Bureau notified the Kansas City meatpacking houses that it could not extend fire insurance coverage to their operations until the city instituted a public sector non-profit water service. The meatpackers convinced the city government to launch a public water system. A system where revenue could fund adequate water pressure unfettered by the need for providing profit to shareholders.

Well into the 20th Century, the NBFU deployed “inspectors” to cities to review firefighting capabilities, building codes, and other fire prevention-related public policies. If an inspection report cited a deficiency in resources or public policy, municipal officials needed to correct the problem – without the niceties of a democratic process – or cartel companies and agents would cease doing business in the city.

In short, the fire insurance cartels wielded authoritarian power. The democratically elected governments answered to the unelected private entities.

No doubt the cartels often used that power to increase public safety, but it remained available for any whim that struck the regional cartels or the NBFU. The only place the fire insurance cartels were not able to wield their power was at the federal level, and that was not for lack of trying.

But that is another story for another time.

Business Harmony

So how did this great mechanism for the concentration of economic and political power begin?

The Civil War in the north demonstrated to American business the value of growth on a national scale. The Union war effort fostered the expansion of great industries. Financiers who funded the expansion understood the higher profits and lower costs available from market dominance.

Just prior to the Civil War, the life insurance sector began marketing the deferred benefit policy on a national basis. Those policies gathered consumers’ capital for insurers’ investment use for decades at a time. After the war and building upon the sale of war bonds as an instrument of investment, life insurers jumpstarted promotion of deferred benefit policies across the country.

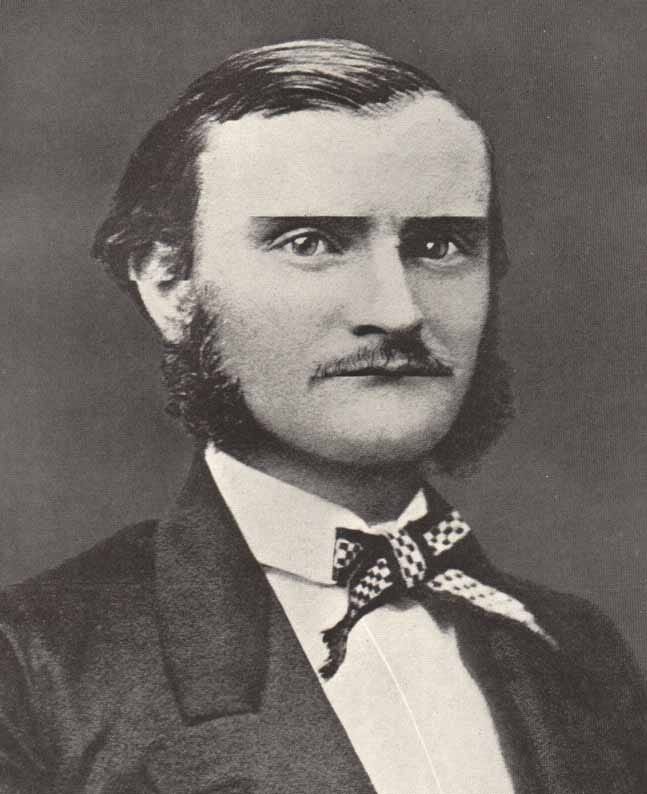

In the realm of fire insurance, a Scottish immigrant and insurance salesman named Alexander Stoddart presented an idea that changed fire insurance and shaped its regulation. In 1863, Stoddart moved to New York City from the Midwest. The next year, he formed a cartel of four companies to privately regulate premium rates and policy forms. From this single act of collusion, a mighty anticompetitive framework arose.

On May 1, 1864, Stoddart's cartel became known as the New York Underwriters Agency (NYUA). Stoddart was not the first to propose an insurance cartel. He may have had dealings with a regional arrangement in St. Louis and eastern Missouri before the war. Still the NYUA was the first insurance cartel with national importance.

From his experience in the Midwest, Stoddart understood that the bond of trust between insurer and insured was weak. Low-ball pricing and policies that over-promised undermined the strength of the industry. Inadequate prices led to insolvency and wild promises went un-kept. In both cases the result was unpaid claims and mistrustful insurance consumers.

Stoddart viewed coordination among insurers and sales agents as necessary to staunch price competition, which Stoddart saw as a threat to insurer solvency.

Insurer financial failures, particularly after urban fires, caused the public to doubt the value of buying fire insurance. The problem was so bad that consumers were advised never to insurer more than 30 percent of the worth of their property with one insurer. A “smart” consumer placed their business with three or four insurers and hoped for the best.

Stoddart put forward a plan that mimicked that consumer approach of dealing with multiple companies. He linked four insurers to stand behind one policy form at an agreed upon rate. Stoddart attacked unfettered competition with the blunt weapon of a cartel.

Today, after 132 years of antitrust law, the term cartel has an odious sound. This was not the case in 1864. Cartels were not only legal, but business and consumers alike saw cartels as a reform. Furthermore, it is important to note, that Stoddart introduced cartel arrangements to fire insurance 5-years before John D. Rockefeller formed the South Improvement Company to bring “harmony” to the petroleum sector.

The introduction of cartel organizations fostered the multi-state insurance business. Cartels could offer lower prices than local insurers and build larger reserves from more diverse sales without succumbing to the “dreaded” price competition among member companies.

The cartel companies quickly attempted to harmonize state regulatory frameworks, which would prove a difficult task. Of course, state officials always cited consumer protection as states crafted regulatory frameworks. Nevertheless, those laws and regulations tended to erect barriers to entry and operation for “foreign” (out-of-state) insurance companies and sales agents. Asking the states to remove those parochial advantages for local businesses was not a welcome request in most state capitals.

In 1866, the NYUA joined with other fire insurance companies to form the National Board of Fire Underwriters (NBFU). The organization coordinated political activities that benefited the formation of fire insurance cartels to impair competition. The NBFU also acted as an insurance cartel organization that generated premium rates and policy forms; although, it rarely exerted full control over the cartel organizations that represented geographical regions of the United States.

Regulatory Harmony

The same year, Stoddart and the NYUA and NBFU initiated efforts in the US Senate to secure passage of federal insurance charter legislation. The legislation would facilitate the circumvention of the parochial rules promulgated at the state level with a federal charter. The fire insurers desired the freedom obtained by national banks in the National Bank Acts of 1863 and 1864 – exemption from state rules and gentle supervision by a under resourced federal office.

When opposition to the bill proved strong, the NYUA initiated litigation challenging Virginia’s authority to regulate insurance. The NYUA assumed that they would triumph in federal court, which would place pressure on the Senate to pass the federal charter legislation. Ultimately, the NYUA attorneys would argue that insurance was interstate commerce; therefore, the Constitution rested jurisdiction over insurance with Congress.

What the NYUA did not consider was that the conservative majority on the Supreme Court were loath to issue any decisions that reduced the powers of states as compared to the federal government. The Court’s conservatives wanted to protect the southern states’ ability to construct systems for White Supremacy. These justices were loath to rule against states.

In 1868, when the Supreme Court ruled in favor of Virginia, the NYUA plan collapsed. The Court ruled the insurance was not commerce, so it could not be interstate commerce; therefore, Congress had no jurisdiction over “the business of insurance.” Insurance was a contract, and states hold jurisdictions over contracts written within their borders.

Not only did the Court’s decision fail to provide the political pressure on the US Senate to pass federal charter legislation, but the decision also removed the ability of any future Congress to pass such legislation.

For the next 60 years, the cartel companies and the life insurance sector brought a series of unsuccessful legal challenges aimed at forcing the Supreme Court to overturn the ruling in Paul v. Virginia. We will examine those efforts together in a future essay.

With the failure of the NYUA’s gambit at the Supreme Court, the NBFU and life insurers turned their attention to the cat-herding exercise of harmonizing state regulatory frameworks.

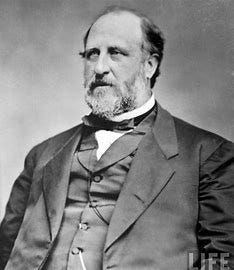

That long, twilight struggle, appears to begin with an intervention in New York State politics by Jim Fisk, Jay Gould, and William Marcy Tweed. In 1870, New York State conducted a gubernatorial election. Tammany Hall, New York City’s Democratic Party organization, led by “Boss” William Marcy Tweed, hoped to turnout a huge vote to order to retain the Governor’s Office and the patronage jobs that went with it. Fisk and Gould financially supported this effort.

History and political buffs love to tell stories about how Tammany Hall ward-heels would take care of their constituents when they ran afoul with the law. The friendly ward committeeman would intercede with the desk sergeant at the local precinct when Pat or Mike enjoyed the local tavern a bit too much on Saturday night.

Tammany’s interventions were not limited to the poor. Take the example of Jim Fisk and Jay Gould. Two financiers and Wall Street manipulators who at robbed railroads of vast wealth and once nearly cornered the gold market. On more than one occasion Fisk and Gould turned to Boss Tweed to get them out of legal jams, in the same way that Pat and Mike turned to the ward committeeman.

The relationship proved vital to the financiers’ ability to escape punishment for their nefarious habits. For example, in 1868, prosecutors charged Fisk and Gould with bribery of the General Assembly. With an intervention from Tweed from “The Wigwam,” a Tammany aligned judge let the two go with little more than a stern warning against the practice of bribing legislatures.

Until the ascent of Al Smith in the early 1920s, Tammany Hall was a business-oriented group. “The Hall” identified issues important to businesses and the former solicited funds from the latter for the former to Get Out The Vote – with the inevitable “monetary leakage” along the way.

Fisk and Gould held stock holdings in life insurers and fire insurers. They also worked with directors and officers from the stock insurance companies on market manipulation operations. It appears, that Fisk and Gould worked with insurers to secure Tammany Hall’s help with “herding cats.”

In the 1870 Election, Tammany Hall delivered a historic vote, which lifted the Democratic Ticket to victory. Governor John T. Hoffman, a former New York City Mayor and Tammany loyalist, won reelection. The governor appointed another Tammany man to the office of Superintendent of Insurance, George Miller.

On February 3, 1871, Superintendent Miller’s first full day in office, he mailed a letter to the chief insurance regulatory official of each state inviting them to New York City in May 1871 to discuss the harmonization of insurance regulations. By the end of that year, the group adopted the name National Convention of Insurance Commissioners (NCIC). In the 1930s, the NCIC would change its name to the National Association of Insurance Commissioners (NAIC).

At the first meeting, Superintendent Miller observed:

The past and prospective increase in the number of State departments, each established under different laws and adopting different forms, rules and regulations has naturally tended rapidly to increase the labor and consequent expense of Insurance companies and, of course, to absorb by so much security or funds of the insured. The most feasible and practicable mode of securing that simplification and unification both of form and of law, which the public interest seems to demand, will be found in concert of action on the part of the several states’ officers charged by their respective states with supervision of insurance.

Clearing the way for the formation of large insurance companies to nationally operate was the motivation behind inviting the insurance commissioners to New York in May 1871. An NAIC history written in 1929 cites an 1870 article from The Insurance Times, describing the industry’s aim for growth: “Companies thus proportioned and managed will in the end and alone survive. We want no other. Pigmies cannot give protection. We need corporative giants to protest us against the ravage of fire and death. We require national insurance companies.”

A future essay will focus on the history of the NAIC.

Fire Prevention

The great urban fires of the 1870s led the insurance industry to take aggressive and organized fire prevention efforts. The most powerful of these efforts came from the NBFU.

After resigning itself to operating under state oversight, and with the help of the NCIC, the NBFU controlled the design of policy forms and premium rates for 20 years. The NBFU ceded this cartel responsibility to a network of local boards and regional associations that worked more effectively under the state system.

In 1892, DeWitt C. Skilton, president of Phoenix Insurance Companies and presiding officer of the NBFU, called for the organization to initiate an active fire prevention program. (The Phoenix took great corporate pride in its standing as the first insurer to pay a claim arising from the Chicago Fire of 1871, according to Chicago newspapers of the time.)

Over the next several years the NBFU developed numerous public policy recommendations aimed at reducing the risk of fire, including a model building code and electrical code. The cartel also drafted the Standard Fire Insurance Law, which most states adopted without amendment.

Insurers encouraged states to appoint designated officers for the prevention of fire during this time-period. Insurance lobbyists pushed for jurisdiction and budget increases for state fire marshal’s offices. To this day, a handful of states still rested jurisdiction over fire prevention and enforcement with insurance regulation in the same constitutional office.

The NBFU worked closely with state and local governments to inspect urban areas and locate fire hazards. This activity became more prominent after major urban fires in Baltimore and Toronto in 1904.

One of the more famous and fateful urban inspections conducted by the NBFU was the San Francisco report published in October 1904.

The City of San Francisco expressed no fear of fire. A major fire 40-years before had led the city to build and support an exemplary fire department. By all historical accounts San Francisco's Fire Department was the best in the country if not the world.

The strength of the fire department made city fathers overconfident. Since officials believed that the fire department could put out any fire, they saw no reason to aggravate property developers with building and fire codes.

San Francisco in 1904 was a compactly constructed wooden city. According to the NBFU inspecting engineers, San Francisco had "violated all underwriting traditions and precedents by not burning up."

Of course, on April 6 of 1906, the city of San Francisco returned to compliance with those "traditions and precedents" after a massive earthquake ignited a conflagration.

San Francisco business and government leaders came to welcome the fire’s destruction. Fire insurance coverage paid for rebuilding many structures found in ashes that were destroyed by shake damage.

In addition, during efforts to rebuild the city, boosters overstated the fire’s destruction to calm the nerves of eastern insurance companies. The deception calmed the anxiety of insurance executives. Underwriters possessed experience assessing risk of catastrophic urban fires but brought very little experience to assessing the risk of shake damage. If San Francisco’s leaders had not succeeded in overstating the loss to fire, insurers may have never returned to the city.

Boycotts & Coercion

The positive aspects of fire prevention activities do not tell the whole story of the fire insurance cartels’ power. And, because of the Paul v. Virginia decision, which found insurance fell outside of Congressional jurisdiction, federal anti-trust laws did nothing to curb that excessive economic and political power.

Some areas of the country did suffer from cartel companies and sales agents. Rural areas of the Midwest and Southwest found it difficult to attract insurance coverage. Either sales agents did not venture into rural areas, or rural sales-leads received bids based on “city rates.” Prices based on urban loss data reflected the higher risk associated with larger urban populations and construction methods. Eastern-based stock-funded insurance company executives did not want to spend the money to secure and service rural business and held biases against rural people.

As a result, progressive populists launched both mutual insurance companies and public-run insurance companies. For example, let’s revisit the activities of the Kansas City, Missouri based William J. Fetter Bureau.

Formed in 1891, The Fetter Bureau controlled the price and policy language of all fire insurance sold in Missouri, except for St. Louis County. (The St. Louis Inspection Bureau, 1893, controlled the business in that county.) The Fetter Bureau belonged to a regional cartel of around 100 companies known as a The Western Union.

As noted above, and drawn from H. Roger Grant’s Insurance Reform, Consumer Action in the Progressive Era, The Fetter Bureau pressured Kansas City Missouri into establishing a non-profit, public water system. The cartel did the same thing in Mexico, Missouri – a small town on the Eastern side of the state. The Mexico City Council issued bonds to pay for the water improvements. But The Fetter Bureau was not satisfied. The fire insurance cartel demanded that the town exempt insurance operations from the city’s business license requirement. When city officials refused to comply, The Fetter Bureau raised the price of fire insurance for all structures in Mexico, Missouri.

In response, city officials took the progressive step of establishing a mutual insurance company to serve the town’s fire insurance needs. The mutual company operated “independent” of the Fetter cartel. (The use of the term “Independent Agent” or “Independent Insurers” survives from those days when some sales agents, brokers, and underwriters remained independent from the cartels.)

Coercion

Wendell Berge’s memo for Attorney General Francis Biddle, available in the Franklin D, Roosevelt Presidential Library, explained anti-competitive weapons the regional cartels used to discipline companies and agents.

“The heavy club used by the board companies to police their rating agreements and to obtain adherence of competitors to such agreements is reinsurance,” wrote Burge. Companies seek reinsurance contracts to transfer the risk of loss off their books, which allows them to write more business than their reserves would usually support. With reinsurance, carriers do not need “to leave money on the table.”

Burge continued: “The rules of the four great regional associations [cartels] prohibit a member company from reinsuring the business of a non-nonmember company. Thus, adherence to fixed rates and charges is assured.”

When disciplining sales agents and brokers, the cartels used “separation” also called the “in or out rule.” Burge explained, “It means that if an agent for one or more board companies undertakes the representation either of an independent stock company or a mutual company, all the board companies acting together will immediately withdraw their business from his office.”

This was the anticompetitive system that prohibited payment for wind damage for the victims of the New England/Long Island Hurricane of September 1938.

Next ….

Part Three: The long battle against the cartels.